Setting Your Initial Capital, Opening Balance and Closing Balance

Initial Capital

If you are just starting your business, you may need to record a special accounting transaction for your initial capital. To do so, you should use "New Accounting Transaction " (available only after enabling CPA mode within User Settings ).

Example:

You are starting your company and investing $10,000.

- Make sure you have your company bank account recorded in OneUp. You can view the list of your banks in the menu "Accounting"

- Next, Open the action, "New Accounting Transaction".

-

Record the transaction as:

- DEBIT: Bank Account 10,000

- CREDIT: "Paid in Capital" 10,000

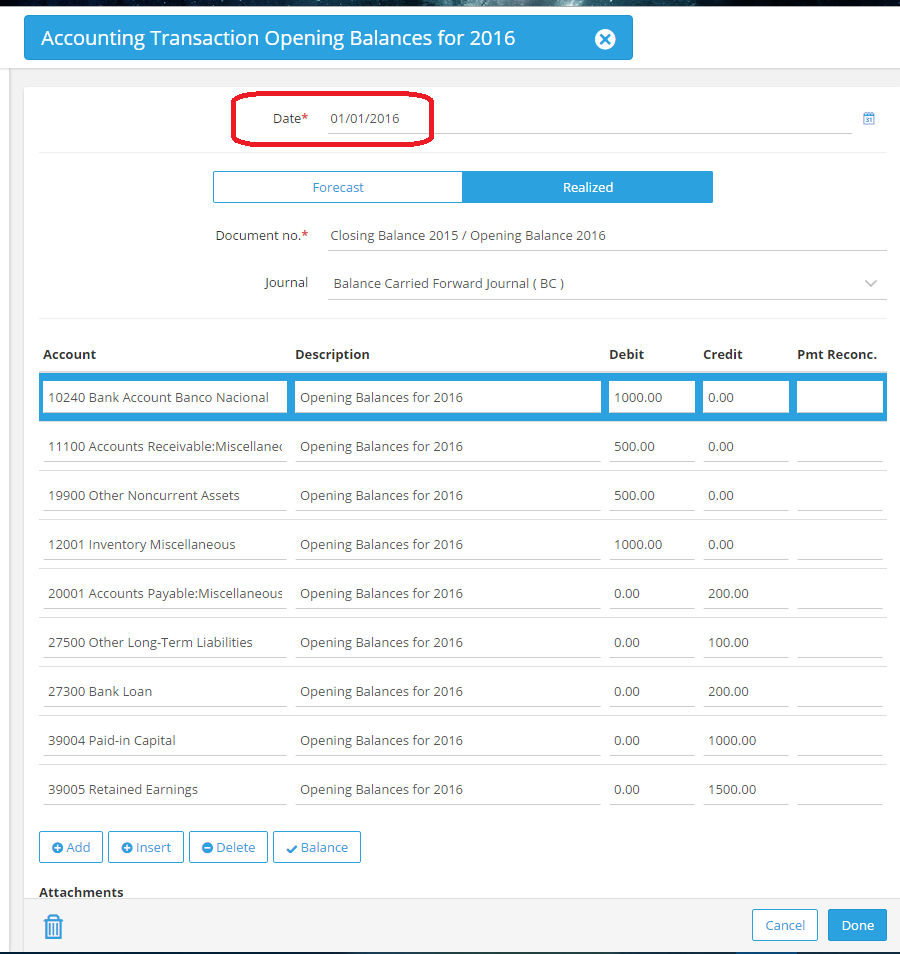

Opening and Closing Balance

| Bank | 1000 | in your favor = debit balance |

| Accounts Receivables | 500 | in your favor = debit balance |

| Other Assets | 500 | in your favor = debit balance |

| Inventory | 1000 | in your favor = debit balance |

| TOTAL ASSETS | 3000 | |

| Accounts Payables | 200 | your debt = credit balance |

| Other Liabilities | 100 | your debit = credit balance |

| Loans | 200 | your debt = credit balance |

| Capital | 1000 | your debt = credit balance |

| Profit | 1500 | in your favor = credit balance (loss would be a debit balance) |

| TOTAL LIABILITIES | 3000 |

Tip:

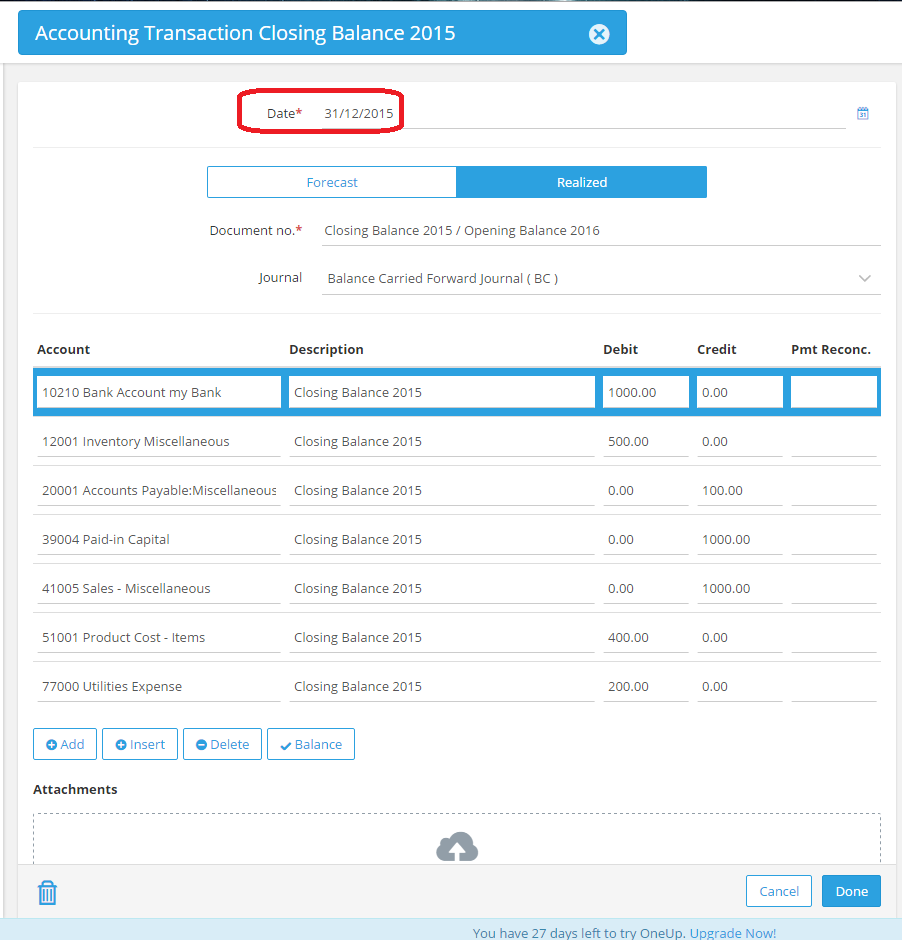

If you need to create an opening balance as of 01/01, but want to set up balance sheet as well as P&L, it might be best to create this accounting transaction for all balances as of 12/31 (previous year) and then use the year end closing, that will allow you to start with opening balances into the new year.

You would then just set up ALL balances from your balance sheet as well as your Profit and Loss Statement. From the nature of accounting, the transaction would be balanced and the year end closing would post your profit and loss into retained earnings for the new year.

You would need to set up your accounting transaction:

- All debit balances from your balance sheet = debit entries in the transaction

- All credit balances from your balance sheet = credit entries in the transaction

- All debit balances from your P&L = debit entries in the transaction

- All credit balances from your P&L = credit entries in the transaction

| BALANCE SHEET | ||

| Bank | 1000 | in your favor = debit balance |

| Inventory | 500 | in your favor = debit balance |

| TOTAL ASSETS | 1500 | |

| Accounts Payables | 100 | your debt = credit balance |

| Capital | 1000 | your debt = credit balance |

| Profit | 400 | not used in the transaction |

| TOTAL LIABILITIES | 1500 | |

| PROFIT AND LOSS STATEMENT | ||

| Sales | 1000 | income = credit balance |

| Cost of Goods Sold | 400 | cost = debit balance |

| Utilities | 200 | cost = debit balance |

| Profit | 400 |

In the example above, you would close 2015 and start 2016 with the opening balances in your balance sheet as of 01/01/2016.

If you create for example an inventory count sheet to generate an opening inventory, you will automatically create an opening balance in your accounting, so, please make sure you do not set up your inventory opening balance in any additional accounting transaction.

The same is valid for bank accounts, if you use the bank entry matching coming from a bank statement for example. For details about bank feeds, please see here: support article

If you create invoices and bills to generate your customer's or vendor's opening balance, you would also already have the according posting in the balance sheet and P&L.

Tip:

If you need to create an opening balance as of 01/01 and include balance sheet and P&L, it might be best to create this accounting transaction for all balances as of 12/31 and then use the year end closing to start with opening balances into the new year.

IMPORTANT NOTE:

The examples in this article are meant as general guidelines only, you should refer to a local CPA who is specialized in local and legal requirements in terms of accounting rules in your country.